WHEN BORROWING against Residential or Commercial properties for investment, it is important to keep in mind the most effective ways of claiming tax benefits, if you wish to maximise the return from your investment.

This is particularly so, when the purchasers are couples — because working with the correct loan set-up can ensure the household tax burden is considerably reduced.

While each case needs to be assessed on its merits as to the most appropriate strategy, there are some general principles that may assist with ensuring your loan is set up correctly. The following list will provide you with a starting point.

1. Assign as much Interest as possible to the higher Income Earner

There are several ways of achieving this. But in terms of loan set-up, the simplest method is to structure the higher income earner as the borrower; with the lower income earner as guarantor.

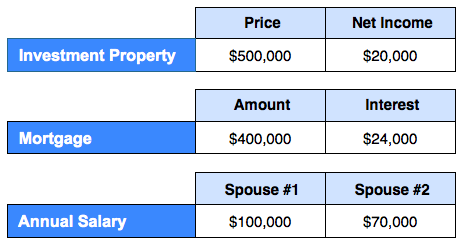

For a couple purchasing in individual names, the loan could be structured in such a way to provide you with the maximum write offs.

In this case, it would make sense for all of the interest to be assigned to Spouse 1. Therefore, a possible structure would be for Spouse 1 to be the borrower, with Spouse 2 providing a guarantee.

But if that did not provide the best allocation of interest to the higher income earner, the loan could be split into two separate accounts — each with an individual borrower, and the other spouse as guarantor.

If the purchase is to be made by a company or a trust, the exact structure would depend on exactly what you are seeking to achieve in each circumstance. And that brings me to the second point.

2. Ensure Your Purchasing Structure is Effective

There are pros and cons in terms of both tax minimisation and asset protection associated with the most common property purchasing structures. These include discretionary trusts, unit trusts, companies and individually — as either tenants in common, or sole proprietor.

Your purchasing “vehicle” should work in concert with the borrowing structure — to produce the best Come in terms of maximising the tax effectiveness of your investment.

3. Get Professional Advice Before Committing to Purchase

You really need to speak with an accountant and/or a financial adviser before committing to an investment property — to resolve the most appropriate structure, and how the purchase fits with your whole financial strategy.

Your debt adviser will be able to offer assistance with possible loan structures to assist with maximising the effectiveness of the purchasing structure.

But it is important to get the right professional advice, to ensure that you fully understand the benefits and risks of your investment.

The appropriate structure may depend on factors such as income distribution within the family, the cash flow to be derived from the investment, the depreciation benefits applicable and your longer-term financial goals.

4. Consider the Worst Case Scenario

While minimising tax is often an important factor when considering borrowing structures, due attention needs to be paid to the potential risks of the investment and how these can be mitigated.

For couples, this is particularly the case, as the purchase of an investment property is usually part of a strategy for setting up the family’s long-term financial future.

Some of the issues involve … market risk, tenant risk (with commercial investments), regulatory risk (the recent discussion regarding the position of negative gearing highlights this as a consideration) and environmental risks.

It is important to have contingencies in place — to mitigate these risks, should the worst case scenario occur. The best place to start would be for you to review? your insurances with a trusted financial adviser familiar with property investment.

Bottom Line: Couples looking to venture into Commercial property investment should ensure they are getting good advice with their acquisition, structuring and funding of every purchase.

Property can be a great way for middle to high-income earners to minimise their tax, while building for their financial future. However, as with any investment, it is important to gather as much knowledge of possible pitfalls before proceeding.

Speak Your Mind