YOU MAY RECALL back in May and July, I foreshadowed a quick recovery would occur – as soon as we emerged from lockdown.

You see, what we’ve just been through, is a medical crisis with financial implications. NOT a total financial collapse – like we had during the GFC.

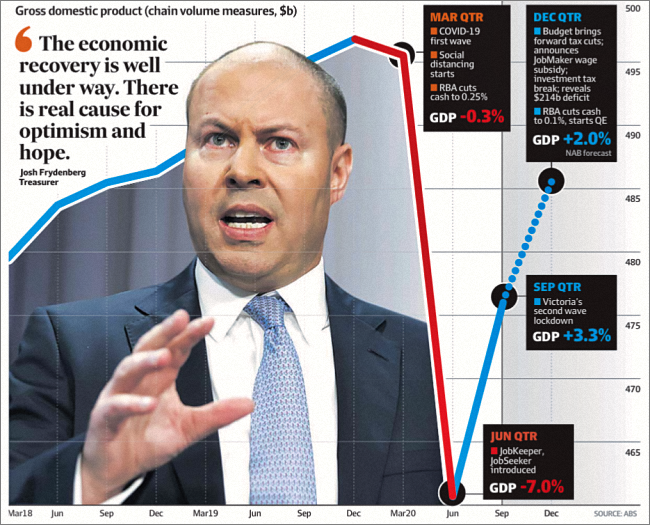

As such, “Demand” didn’t disappear … it simply got deferred. And you’ve already observed that with consumers now engaging in “Retail revenge” – as depicted in the graphic below (AFR, front page: 3 Dec 2020).

During the pandemic my clients seemed to fall into two camps:

- Those who feared a total collapse, with a prolonged recovery.

- Those who listened and saw the opportunity to secure a good property, while the market itself remained confused.

Already you are seeing eager buyers re-entering the property market (both residential and commercial) – with prices on the rise once more.

Therefore, those who did buy during the pandemic are now having their faith vindicated. And now, the strength of this renewed demand is bringing more properties onto the market.

Therein, Lies Your Next Opportunity

Not all the properties coming onto the market during November & December can be absorbed before Christmas.

Naturally, this will make those vendors somewhat unsettled – because the commercial market doesn’t officially reopen again until February/March.

So, if you are cashed up and able to move quickly … there should be a number of good choices for you early in the New Year.

Bottom Line: What I’m planning to do is compile a list of those unsold properties for my clients. And then, we’ll quietly sift through these opportunities together – to help clients secure several genuine bargains.

If that could be of interest to you … just let me know.