In several previous postings, you’ll recall that I have raised the issue of Australia’s current blowout in household debt.

A recent article in the weekend Financial Review (pages 26-27) highlighted the current state of affairs.

While Australia’s overall direct exposure to the US sub-prime crisis is low … it is still having an indirect effect on the cost of money for our Banks.

While Australia’s overall direct exposure to the US sub-prime crisis is low … it is still having an indirect effect on the cost of money for our Banks.

And, quite apart from the Reserve Bank’s actions, this is causing our local interest rates to rise even faster.

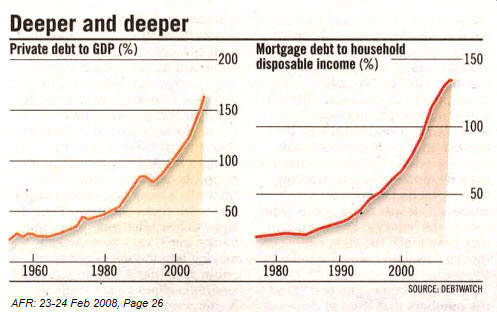

We have now reached the point where:

* The average family will spend 12% of its annual income, just to meet mortgage payments.

* Private debt has risen from 40% of disposable income (in 1996-67), to the current level of 160%.

* Australia’s total private debt is now approaching $1.8 trillion — compared with our gross domestic product of less than $1.1 trillion.

How does that affect Commercial Investors?

If you’ve heeded my warnings over the past 3 to 4 years, you will have restructured your personal borrowings and locked-in your interest rates.

And by now, you may well have cashed in some of your shares.

Therefore, within the Commercial Markets that are NOT over-heated … you are probably now well placed to take advantage of some investor hesitancy, due to rising interest rates.

Let me explain:

You’ve decided to purchase a Commercial property and borrow on a Loan to Value Ratio (LVR) of 70%, at a fixed interest rate of (say) 9% per annum.

However, your interest payments represent only 6.3% per annum [ie: 9% x 70%] of the actual purchase price.

Therefore, if your property is well let and returning you (say) 6.75% per annum net … then, you could still achieve a positive cash flow, and also enjoy the expected capital growth.

So, rising interest rates need not prevent you from still acquiring well-let Commercial Properties. You simply need to structure your borrowings to at least ensure it remains more or less cash-flow neutral.

That way, you would be shielded from any further rate rises.

And in the months ahead, you simply need to adjust your LVR to make sure your interest bill equates to the net return from your chosen property — at the time of borrowing.

So, there is no reason to interrupt your investment plans. Just be more selective in how you filter your properties; and be more astute in structuring your finance.

And that way, you’re able to sleep soundly — being shielded form further rate rises.

Speak Your Mind