.

THIS IS CERTAINLY a two-speed story, according to the Property Council’s most recent Office Market Report.

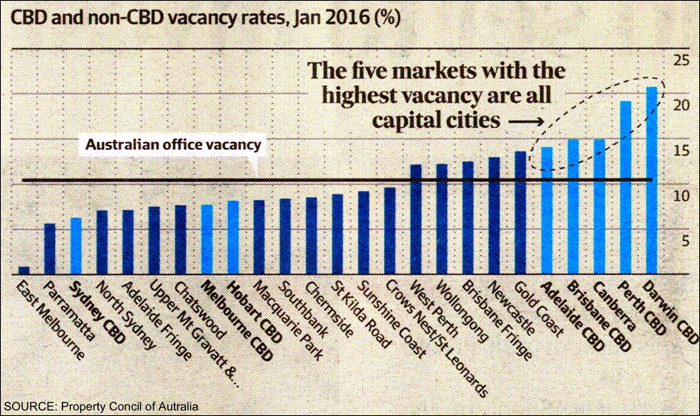

The vacancy rate in Perth currently sits at around 20%; with office rentals down about 40% since there 2012 peak.

Sydney saw a 100,000 sqm take-up in the 12 months to December — which is three times its historical average. And the demand for office space was also strong for Melbourne.

At the same time, the Brisbane, Perth, Canberra, Adelaide and Darwin markets are languishing — with vacancy rates ranging from 14% to 21% of available space within those markets.

CBD Office Cycles No Longer Coincide

Last century, all Australian CBD office markets appeared to transition through a similar boom-and-bust cycle. And it seemed to last for more or less an 18-year period, from peak to peak.

However, all that has now changed. And there are two main reasons for that.

“Hidden” Opportunities

Over the past 20 years, both Sydney and Melbourne undertook major urban renewal projects adjoining their CBDs — namely Darling Harbour and Docklands.

These projects allowed a number of private developers the opportunity to attract pre-commitments from major tenants, who no longer felt the need to be situated in the heart of the CBD.

As a result, this allowed the CBD tenants (like lawyers, accountants, merchant bankers, etc) to expand and back-fill the vacant space within the vacated buildings. Rather than expanding to a point where they needed to move out of those buildings — which would have then fuelled a speculative building boom, at the end of the traditional 18-year cycle.

The Global Financial Crisis

In the lead up to the GFC, Brisbane and Perth saw a large number of speculative office projects, as a result of the localised growth accompanying the huge mining boom in those states.

While economic growth was abruptly halted by the GFC, thee numerous office projects (which were already underway) remained years from completion. And this is what is now responsible for their 15% and 20% vacancy rates, respectively.

Sure, the GFC saw the Melbourne and Sydney office markets dipped slightly — Sydney perhaps more so, because of its heavy tenant weighting towards the financial sector.

However, with the absence major speculative building projects, these CBDs quickly bounced back — having vacancy rates currently at 6.3% for Sydney, and 7.7% for Melbourne.

Bottom Line: If the notion of an 18-year cycle still holds true, Sydney and Melbourne probably reached their cycle midpoint in 2010-11. Whereas Adelaide, Brisbane and Perth are only now progressively reaching their midpoints.

As such, Australia’s CBD office markets are no longer running in-sync. And as an investor, you need to be mindful of just where you are within the specific CBD cycle right now.

Adelaide is approaching its bottom, and will probably flat-line for a year or two. However, Brisbane and Perth have not yet bottomed out — given their vacancy rates are 14% and 20% respectively.

Besides, Melbourne and Sydney are far more mature CBD office markets. Therefore you’re better served by focussing on these two capital cities.