There has been much made of the poor US Retail Sales Data for December.

However, the figures were only down 0.4% on November. The most likely explanation being that some early Christmas shopping occurred November; and the increase in gift-card sales will not come through until early in 2008.

Clearly, the Sub-prime issues are having some effect. But, if you follow HS Dent at all — their view is that … “a short, mild recession is indeed likely, and we are arguably already in the middle of it.” (Update: Wednesday 16 January 2008).

Therefore, things ought stabilise for the US by mid-year … particularly, with the Federal Reserve’s intervention.

And one other annalyst I was reading quipped something to the effect that … “Wall Street had managed to predict seven of the last two major recessions!”

So, the general consensus would appear to be that things have reached “irrational levels of pessimism”.

Global View

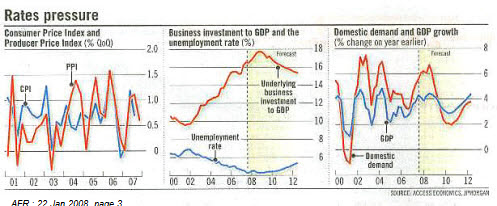

Despite all this widespread pessimism, the global economic outlook is generally good — with Asian growth basically decoupled from the US, and the outlook for China strong.

Likewise, Australia is far less dependant upon the US — who took less than 6% of our total $168 billion in exports, compared to China’s share of over 15%.

Two years ago, the US and China each took about 10%. Now, the US share equates to that of New Zealand. And China is now second only to Japan as the major buyer of our exports.

As a result, Australia’s economy grew at around 4.3% to September last year. And total private sector demand expended by 6.2% over the 12 month period.

As a result, Australia’s economy grew at around 4.3% to September last year. And total private sector demand expended by 6.2% over the 12 month period.

What next for the RBA?

On balance, this still provides our Reserve Bank with compelling reasons to increase rates at the beginning of February. And probably do so at least once more during 2008.

Even so, this should have little influence upon Commercial property overall. The main affect of any rate rises will be felt by residential property, in many of the outer suburbs around the country.

Speak Your Mind