DESPITE THE RECENT new Omicron variant, consumer demand is surging against the backdrop of labour shortages, supply chain blockages and recent price increases.

All of this is causing confusion and some concern. And pundits around the world are detailing strong Inflationary pressure – which usually means interest rates are likely to increase, sooner rather than later.

However, the Reserve Bank of Australia believes we may have seen the worst of the Covid impact upon consumer prices. Anyhow, here are several guiding signs for you to watch.

Easing Supply Chains

Every day, we hear about difficulties in sourcing retail goods and other materials. And the transport drivers’ disputes are certainly not helping things – especially in the run-up to Christmas.

Nonetheless, there is a suggestion that these difficulties and delays are starting to ease.

Rising Housing Costs

These tend to make up about one-third of the Consumer Price Index – and have disproportionately risen over the past 12 months.

These tend to make up about one-third of the Consumer Price Index – and have disproportionately risen over the past 12 months.

However, these might now be starting to ease as well.

You regularly saw clearance auction rates of 75% to 80% through 2021 – which consequently caused a surge of between 20% and 25% in house prices, and even more in some locations.

Although, over the last couple of weekends, you’ve seen clearance rates closer to 60% – which would tend to reflect a more “balanced” residential market.

Commodity Prices and Energy

The prices of commodities like copper look as though they have begun to stabilise. Plus, the price of oil appears to be easing to around $US80 as we enter the New Year.

General Consumer Sentiment

How people feel about inflation it’s clearly important.

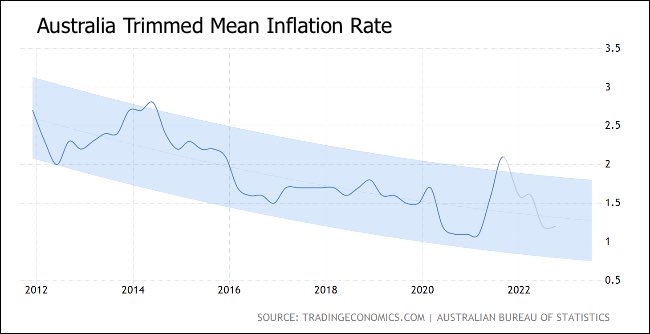

You recently saw the Trimmed Mean (Underlying) Inflation Rate rise to slightly above 2% in the September quarter. Yet, as you can see, the prediction is for it to consolidate back just above 1% annually during 2022 – suggesting this was probably only a temporary rise in Australia’s overall inflation rate.

And this tends to support the Reserve Bank’s wait-and-see strategy towards prematurely raising interest rates.

Bottom Line: Basically, people have been playing catch up following the long and frustrating hibernation. And the economy simply needs time to readjust to the “new normal”.

As such, the outlook for commercial property looks solid over the next few years. And we should probably take more heed of the measured approach being adopted by the Reserve Bank.

Speak Your Mind